Federal Reserve Predicts Mild Recession in US

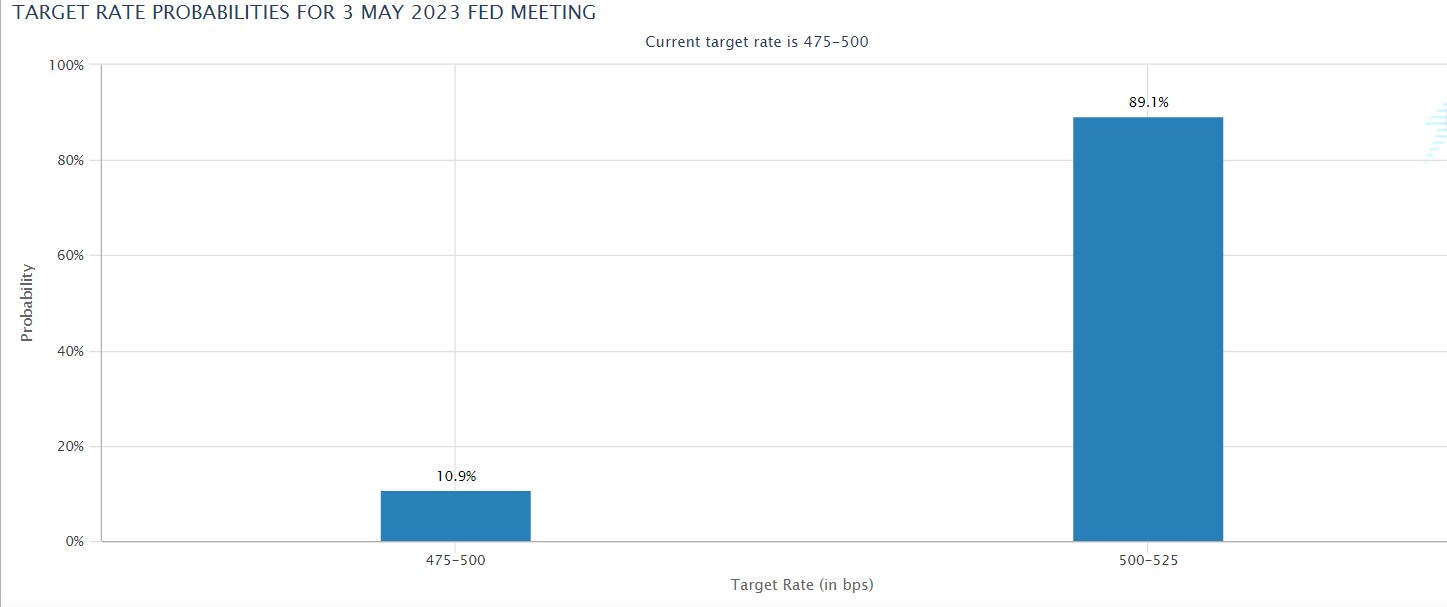

Futures Pricing in Almost 90% Chance of FED Interest Rate Increase.

Here is what we will be getting into today:

FOMC & Market Notes

Foreign Currency Risk

Let's Dive In!

Fed Policymakers Predicting Recession In The US

US equity markets have been volatile in recent weeks due to several factors, with investors spooked by the Federal Reserve's latest monetary policy meeting. The minutes from the March meeting revealed that policymakers predicted a mild recession in the US, starting later this year. Several members of the Federal Open Market Committee considered freezing interest rates following the turmoil in the banking sector in the run-up to the meeting, but the FOMC decided to press ahead with a quarter-point rise to a new target range of 4.75% to 5%.

Investors have been weighing up the potential for more interest rate rises from the Federal Reserve, following labor data showing the continued strength of the US labor market. Despite adding fewer new positions in March compared to February, the US economy still added 236,000 new positions, which was not enough of a slowdown to discourage the central bank from making another rate rise to tamp down inflation. Futures markets are now pricing in an almost 90% chance of an interest rate increase at next month's meeting.

Inflation data illustrated that the central bank's aggressive tightening of monetary policy was bringing inflation down towards its 2% target, with the consumer price index rising 5% last month, compared with 6% in February. Core inflation, which strips out volatile food and energy costs, rose 5.6% year on year in March, suggesting prices remained elevated in parts of the economy. Citi analyst Stuart Kaiser said that consumer price inflation is expected to dip to an annual rate of about 5.2% and a month-on-month rate of 0.3%, which would mark modest deceleration but remain too high for comfort and likely read negative for stocks.

Corporate America is expected to face its sharpest drop in profits since the early stages of the pandemic, according to Wall Street forecasts. Analysts predict that companies on the S&P 500 index will report a 6.8% decline in first-quarter earnings compared to the same period last year, due to high inflation squeezing margins and fears of an impending recession holding back demand. Despite recent turmoil in the US banking industry, the financials sector is expected to report a 2.4% increase in profit and lead all sectors in revenue growth at 9.1%.

Chinese exports surged last month, fueled by sales of electric vehicles and their components, despite weak global growth. Customs data showed dollar-denominated exports expanded 14.8% in March compared with the same period a year earlier after falling 6.8% in January and February.

Currency Risk Poses a Billion-Dollar Blind Spot

The International Monetary Fund (IMF) has urged seven of the world's largest economies to bring their government borrowing under control to help fight against high inflation and financial instability. The countries identified are Brazil, China, Japan, South Africa, Turkey, the UK, and the US. Gaspar, the IMF's head of fiscal policy, warned that these countries are likely to push public debt up by more than 5% of gross domestic product over the next five years. He also stated that by 2028, the world's public debt burden was on course to match the value of goods and services produced in the world.

Gaspar urged advanced economies and the largest emerging markets to take action to reduce banking turmoil and control inflation by taking charge of their finances. He suggested that implementing fiscal tightening measures could help to moderate the growth of aggregate demand and thus contribute to more controlled increases in policy rates. This, in turn, would alleviate the pressures on the financial system caused by the spike in borrowing costs that occurred during 2022.

Debt restructuring has become increasingly complex with more players, less transparency, and complicated instruments involved, making it crucial to prevent the need for such restructuring. In low-income countries, primary deficits and exchange rate depreciations remain the primary drivers of debt accumulation. Exchange rate risk was a key factor in the Asian debt crisis, the LatAm debt crisis, and many if not most emerging market crises. Currency risk is the most unpredictable and largest driver of upward debt dynamics but has not been identified by the World Bank/IMF as a problem worth solving. This is a billion-dollar blind spot that should be tackled before it turns into a trillion-dollar debt crisis.

The World Bank and IMF have prioritized their focus on climate finance and the debt sustainability of low-income countries. The problem with this is that countries facing debt distress are unlikely to borrow funds to invest in green infrastructure. In other words, debt becomes the primary concern while climate becomes secondary.

China's lending spree to developing countries and refusal to play by western-established rules represents the single greatest impediment to government debt workouts and threatens to leave some countries in debt limbo for years. Many of these loans are opaque in size, terms, nature, and sometimes even existence. It is difficult to determine the total extent of China's lending programs, as a significant portion of their loans remain unreported.

In February, the IMF announced the formation of a Global Sovereign Debt Roundtable with the goal of bringing together all parties involved in the debt resolution process. It is essential to address currency risk in debt dynamics to prevent potential crises.

For more analysis on these topics, check out these articles:

Fed Rates

Currency Risk

Public debt could return to pandemic-era high, warns IMF fiscal chief

Its the currency, stupid (part 2): is the lowest hanging fruit forbidden?

How to slash sovereign debt burdens

Chinas AIIB calls for multilateral lenders to keep prized preferred creditor status

Sri Lanka central bank says sovereign lenders yet to outline debt talks plans

Thanks For Reading!

If you find value in this newsletter and want to make sure you don't miss any important updates, you should definitely consider subscribing. By subscribing, you'll be the first to know about new articles and special offers.

We also offer a paid service which will give a breakdown of every source we cover that will be sent out almost daily.

Our Wednesday newsletter will always be free, but to make sure YOU are not missing anything be sure to sign up for our paid subscription.

If you have any newsletters you wish to see in our lineup, please reach out and let us know. We will continually look to incorporate more sources to our weekly wrap-up.