OPEC's Production Cuts Fail: Oil Prices Continue to Slide.

Commodities All Falling

OPEC's Dilemma and the Future of Shale Production

OPEC and its allies have made two significant production cuts since October in an attempt to prop up oil prices. These cuts have not been successful, as prices have continued to decline. The International Energy Agency (IEA) and OPEC predict that the market will tighten significantly in the second half of 2023, which should boost prices. However, traders seem unwilling to believe this prediction, and prices have only rallied briefly before slipping lower again.

One reason for this lack of confidence may be the approach taken by Saudi Arabia's oil minister. His management of the oil market has been praised for reinforcing Saudi influence over the oil market and its OPEC+ alliance with Moscow. However, his tendency to overplay his hand and pick unnecessary fights has made his central role in managing oil prices more challenging. His recent decision to exclude news organizations from OPEC meetings has been seen as a sign of desperation as Saudi Arabia struggles to control falling oil prices.

Energy Policies

The Biden administration has implemented over 150 policies that have made it harder to produce oil and gas in America. These measures include a moratorium on new oil and gas leases on public lands and offshore waters, the elimination of federal fossil fuel subsidies, and rejoining the Paris Climate Agreement. These policies have artificially raised the regulatory costs of fossil fuel energy production and encouraged capital withdrawal from the domestic oil and gas sector. The Institute for Energy Research (IER) warns that these policies will make the US import more petroleum products from countries such as China and the Middle East.

OPEC+ Members & Russia

OPEC+ is facing intense downward pressure on oil prices due to several factors, including Russia's petroleum exports remaining higher than anticipated, slower economic rebound in China, weakened manufacturing and freight activity in North America and Europe, persistent inflation, and the U.S. regional banking crisis.

While Saudi Arabia leads OPEC in its efforts to stabilize oil prices, there is no guarantee that Russia and other OPEC+ members will follow suit. Moscow is trying to maintain its exports despite Western measures designed to restrict energy revenues flowing into its war chest. One option to strengthen the position of countries in the long term is to alter production baselines for OPEC+ members.

Weaker members of the OPEC+ group, including Nigeria and Angola, are struggling to meet existing output targets and are hesitant to make deeper cuts. Nigeria has even expressed a desire to increase its own production target. Talks with other producers, including Russia, could also be complicated by a desire to raise production baselines for some members, chiefly the UAE, which has long sought a higher baseline to reflect its growing production capacity.

End of a Revolution

The shale revolution has had a significant impact on global energy markets, with shale oil production in the US rivaling that of Saudi Arabia. The shale revolution basically refers to a special technique that improved the ability to extract oil and natural gas from the ground. This era of rapid shale growth is now coming to a close. Specifically, the Permian basin in West Texas, which has been the primary source of growth in recent years, is approaching its peak production level. The most favorable drilling locations have been exhausted, and producers are now compelled to operate in lower-quality areas, resulting in diminished output.

Seismically active areas and mountainous regions make it difficult to produce shale commercially, limiting the potential for shale oil and gas production worldwide. The UK's Gatwick Gusher did an initial test well, but did not yield commercial production due to geological limitations. Argentina has good shale potential, but regulatory issues and difficulty getting capital out of the region make it challenging.

The future oil production growth will have to come from deep water offshore wells that are more expensive. While there may be other potential shale plays in other countries, such as Russia, there are significant impediments to shale production in those countries. The resource markets in the oil markets are cyclical, and at some point, production will be coming online probably at exactly the wrong time when it's not needed, and prices will fall.

Renewable Energy & ESG

Global orders for new wind turbines are up almost 30% year over year & hit a record in Q1 2022. China accounted for more than half of the activity. Latin America had a record Q1, thanks to activity in Argentina and Brazil, and the US is seeing renewed confidence and order growth, partially thanks to the Inflation Reduction Act. Renewable energy capacity is set to grow by one-third in 2023, as forecasted by the International Energy Agency.

This transition from fossil fuels to renewable energy is not without challenges. The shift involves going from a system dominated by liquid and gaseous hydrocarbons to one dominated by solid minerals and rocks and metals. This requires a significant increase in the quantity of minerals and metals that have to be mined, which is done with oil-burning machines. Additionally, the resins used to make wind turbine blades are produced with hydrocarbons, and concrete and steel require metallurgical coal, natural gas, and oil.

Supply side problems are affecting most commodities, including copper, nickel, cobalt, and lithium. Politicians' plans for ESG initiatives are not feasible due to the shortage of key metals required to replace oil & gas. Resource nationalism is becoming more real, and the world is going back to a little balkanization, where trading blocks are formed.

Traditional forms of energy such as oil and gas remain essential due to their energy density and the limitations of renewable energy sources. The neglect of upstream investment in oil and gas for the past decade or more has led to shortages, which will likely worsen in the future.

Nuclear power may be a viable alternative to traditional forms of energy, but there are currently significant challenges to its implementation. The energy infrastructure is becoming increasingly fragile due to the lack of investment in the space for the past 15 years. The 2022 energy crisis was a warning sign, highlighting the scarcity of resources and the abundance of cheap, reliable base load power.

Investor Sentiment and Portfolio Allocation

In the long term, commodities are traditionally the best inflation hedge and have outperformed stocks, bonds, and real estate in past inflationary cycles. The resources world is always a cyclical business, and too much money comes in, chases projects, and underwrites them at high prices, leading to price collapses. Traditional value investors such as David Einhorn and Warren Buffett have been adding coal, natural gas, and oil stocks to their portfolios due to attractive valuations.

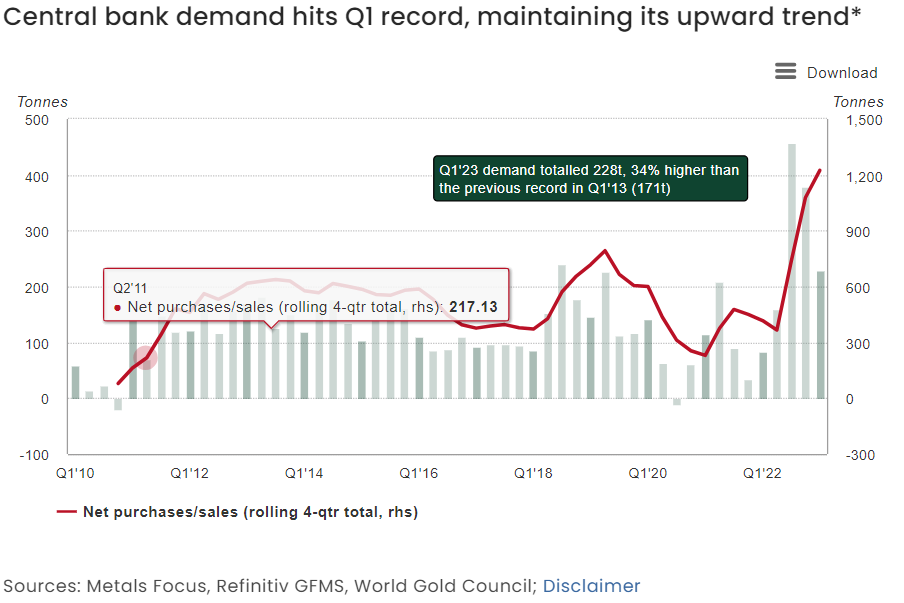

OPEC, Dollar, and Gold

The de-dollarization theme is gaining traction recently, and could be the catalyst for a new cycle. The US dollar may not collapse, but even a shift on the margin would be historically coincident with a massive re-rating in gold and in commodities relative to financial assets. Central banks have become massive gold buyers, and this trend is likely to continue going forward.

Whatever replaces the US dollar as a reserve currency or as a monetary system will probably have a gold component to it. Gold convertibility could be the way to settle some of these surpluses and deficits. This would start an unbelievable market for real assets. The lack of investment in the commodities space is starting to have a significant impact on production, while demand remains strong. Historically, every major period of commodity cheapness relative to financial assets has been resolved by commodities moving much higher. The trigger that re-rated commodity prices from radically undervalued to ultimately radically overvalued was a shift in the global monetary order.

For more analysis on these topics, check out these articles:

Adam Rozencwajg: Oil & Energy Has The Cheapest Valuations In The Entire Commodities Complex?

150 Ways Biden Has Made It Harder to Produce Oil and Gas: Energy Institute Report

Saudi Arabias prickly prince of oil bristles as crude price slides

With Oil Prices Slumping, OPEC+ Producers Weigh More Production Cuts

Thanks For Reading!

If you find value in this newsletter and want to make sure you don't miss any important updates, you should definitely consider subscribing. By subscribing, you'll be the first to know about new articles and special offers.

If you have any newsletters you wish to see in our lineup, please reach out and let us know. We will continually look to incorporate more sources to our weekly wrap-up.