Government Shutdown

Fed Pauses, Recession Risks

Government Shutdown

A potential government shutdown looms due to the failure of Republicans and Democrats to reach a deal on new spending legislation could have far-reaching consequences. Government shutdowns have occurred in the past, with the first significant ones taking place during Bill Clinton's presidency. The longest government shutdown in history happened between 2018 and 2019 when then-President Trump and congressional Democrats entered a standoff over funding for a border wall. This disruption lasted 35 days but was only a partial government shutdown as some appropriations bills had already been passed to fund certain government functions.

Before Article Market Predictions:

In previous instances, the government has been reluctant to reduce expenditures, even in the face of rising core and headline prices. To mitigate the potential economic fallout from a shutdown, it is crucial for the government to cut unnecessary spending and significantly reduce the deficit. Implementing more government stimulus plans could exacerbate existing problems of a low-growth, high-debt, and poor-productivity economy.

To end a government shutdown, it is the responsibility of Congress to fund the government. The House and Senate must agree on funding, and the president must sign the legislation into law. This process is typically time-consuming and may not be resolved until December at the earliest.

The shutdown possibility has led to the proposal of the Prevent Government Shutdowns Act. This bipartisan bill aims to ensure that Congress completes its work on all 12 appropriations bills needed to fund the government. It proposes implementing 14-day continuing resolutions to keep the government funded at the previous year's levels while Congress focuses on passing appropriations bills.

Approximately 4.5 million federal employees may not receive pay during a shutdown, although they are entitled to back pay once the government reopens. Essential services like Treasury debt payments, Social Security checks, and mail delivery would continue, but routine operations such as food inspections and small business loan approvals could temporarily halt.

In the past, a five-week partial shutdown resulted in the furlough of approximately 300,000 federal workers. This had a negative impact on economic output, with a 0.1% reduction in the fourth quarter of 2018 and a further 0.2% reduction in the first quarter of 2019. The 2019 five-week partial shutdown resulted in an estimated $11 billion in lost economic activity, with $3 billion unlikely to be recovered. A current government shutdown could reduce annualized GDP growth by 0.2 percentage points each week, according to Goldman Sachs.

The Federal Reserve

In its September meeting, the Federal Reserve maintained interest rates at their current level, signaling the end of the current hiking cycle. Despite no rate hikes, the Federal Reserve announced its intention to continue reducing its balance sheet. The Fed aims for a unique achievement: a slow rate-cutting cycle that will result in a soft landing for the economy. The central bank plans to gradually reduce rates over the next three years, as inflation slows down and job losses remain minimal. Historical data suggests that this approach may not be as effective as anticipated. Interest rates tend to rise slowly but decline rapidly. In almost every interest-rate cycle, there is a period of rapid rate cuts. The Fed's current forecast of a prolonged series of rate cuts goes against this historical trend.

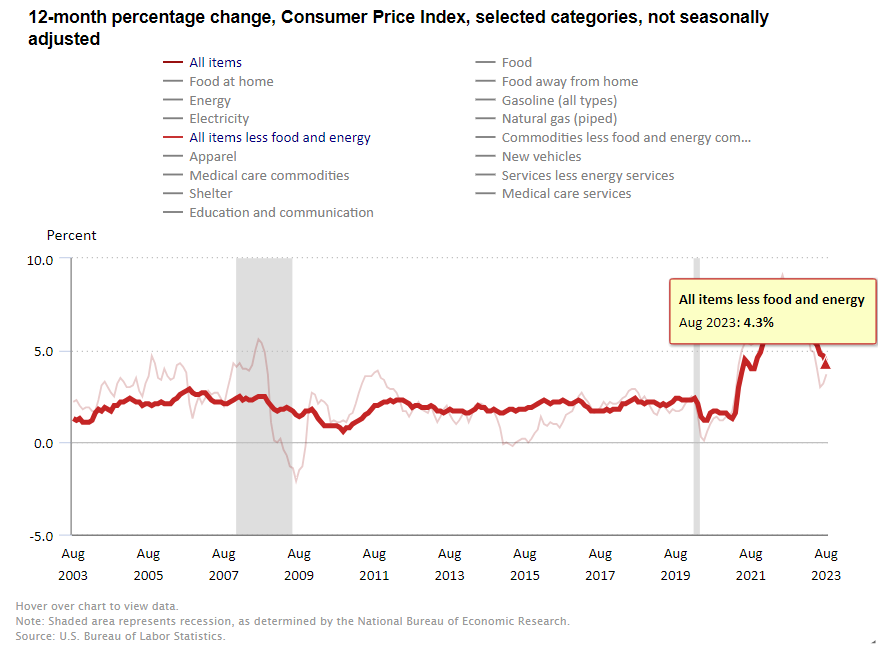

Despite inflation gradually cooling, it remains above the target 2% level in most large economies. Policymakers forecast that inflation, after excluding food and energy prices, will ease to 3.7% by the end of this year before falling to 2.6% and 2.3% in 2024 and 2025, respectively. As of August the core cpi stands at 4.3%. Even with inflation cooling the press conference has led to expectations that the Fed is unlikely to raise rates further this year, unless there are significant upside surprises in inflation data. Market pricing reflects this sentiment, with a 28% chance of a rate hike in November, slightly lower than the previous day's 29% chance and significantly lower than the 41% chance seen a week earlier before the September meeting.

Recession Risks

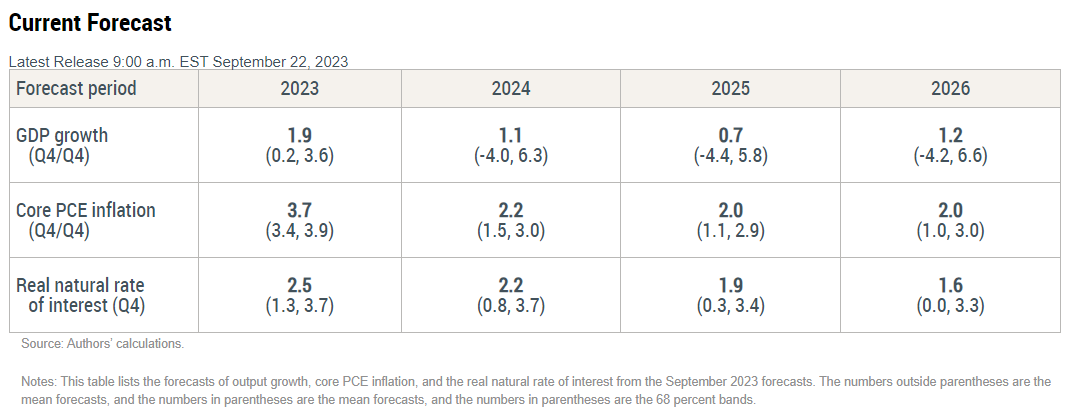

The Federal Reserve Bank of New York's dynamic stochastic general equilibrium (DSGE) model provides insights into potential recession risks. The model forecasts that despite an increasingly restrictive monetary policy stance, the U.S. economy remains resilient. The probability of a not-so-soft recession, defined as four-quarter GDP growth dipping below -1 percent by the end of 2023, has significantly decreased from 26 percent in June to just 4.6 percent.

However, the U.S. is currently experiencing a private sector recession masked by excessive government spending. The services sector and consumption are being supported by increasing levels of debt. In July 2023, the personal savings rate was only 3.5%, well below the pre-pandemic average of 6.9%. Furthermore, total credit card debt surpassed $1 trillion for the first time ever in the second quarter of 2023, contributing to a record total household debt of $17 trillion.

The United States is also facing a rising government deficit, which reached $2,474 billion, accounting for over 9% of the country's GDP of approximately $27,000 billion. This increasing debt is currently propping up the GDP, but it is also leading to elevated inflation expectations.

Another recession indicator is suggesting recession. This indicator is the spread between the University of Michigan's Index of Consumer Sentiment (UMICS) and the Conference Board's Consumer Confidence Index (CCI). Historical data suggests that when the spread between these two measures widens and then begins to narrow, a recession is likely. Currently, this spread is narrowing, suggesting an impending recession.

The United Auto Workers (UAW) are currently on strike. The initial impact of the limited strike is expected to be modest, but a broader work stoppage could curtail auto production and lead to higher vehicle prices. Furthermore, the strike delays the auto sector's full recovery from supply-chain disruptions caused by the Covid-19 pandemic, potentially leading to reduced output and higher prices.

The resumption of federal student loan payments on October 1st could divert around $100 billion from Americans' pockets over the next year. The pause in student loan payments since March 2020 allowed borrowers to allocate that money towards other expenses, thereby supporting economic growth. However, the resumption of these payments could potentially impact major retailers.

Adding to the financial pressure is the increase in gasoline prices. Brent crude oil prices have risen above $90 a barrel in recent days, up from just above $70 earlier this summer. This surge is not due to an increase in demand, but rather a result of supply constraints. Historically, such spikes in oil prices have often led to economic downturns, particularly in economies that are already struggling. The current surge in oil prices is likely to have a similar effect.

Market

The Fed's cautious approach to rate hikes has been met with mixed reactions from the market. The 10-year Treasury yield spiked to 4.41% after the press conference, and stock prices fell, with the S&P 500 index down 0.9% and the Nasdaq Composite down 1.5%. This reaction reflects the market's uncertainty about the future economic outlook and the potential impact of higher interest rates on investment returns.

Goldman Sachs has warned its clients about the possibility of a volatility eruption in the near future. According to John Marshall, a derivatives strategist at Goldman Sachs, October could be the month when these risks materialize and result in a decline in stocks and an increase in options volatility. To hedge against expected stock market weakness, Marshall suggests that clients consider buying October call options on the Cboe Volatility Index (VIX).

After Article Market Predictions:

For more analysis on these topics, check out these articles:

The New York Fed DSGE Model Forecast September 2023

US government heads for shutdown as Republicans squabble over spending

How a Shutdown Could Affect You

When Rates Drop, They Usually Plunge. The Fed Thinks Different.

A New Wave of Stock Market Volatility Could Be Right Around the Corner. What to Do.

The Outlook: U.S. Economy Could Withstand One Shock, but Four at Once?

The U.S. could be in a recession and we just dont know it yet

Good News: We Can Expect More Recessions in Future

Treasury Yields Arent Done Rising. Buy Them Anyway.

Federal Reserve hardens commitment to higher for longer interest rates

The Fed Is Unsure About 2024. Why Thats a Problem for Markets.

Surveillance: JPMorgan Sees Fed in Uncomfortable Jam Into 2024

Shutdown, Strikes, Sticky Inflation, and More Brace for a Bumpy Fourth Quarter

The Fed Is Curbing Inflation, But Consumers Say Theyre Still Paying Too Much

The Feds Dot-Plot Told One Story. Powell Gave Us Another.

WARNING! Another Economic Time Bomb Just Exploded

Its Time to Rethink the Recession

Peter Schiff: Jerome Powell Is Just Guessing

Why traders aren't buying the Fed's 'higher-for-longer' vision

The Dangerous Myth Of Soft Landing

Lets debunk the bears top arguments against further stock market gains

The federal government is headed into a shutdown. What does it mean, whos hit and whats next?

Carefully, Dude: Powell at the Press Conference

Global central banks unite in "higher for longer" credo

Novel Approach Would Avoid Government Shutdown

Heard on the Street: Dont Buy the Federal Reserves Rate Projections

Thanks For Reading!

If you find value in this newsletter and want to make sure you don't miss any important updates, you should definitely consider subscribing. By subscribing, you'll be the first to know about new articles and special offers.

We also offer a paid service which will give a breakdown of every source we cover that will be sent out almost daily.

Our Wednesday newsletter will always be free, but to make sure YOU are not missing anything be sure to sign up for our paid subscription.

If you have any newsletters you wish to see in our lineup, please reach out and let us know. We will continually look to incorporate more sources to our weekly wrap-up.