Is the Housing Market Maintaining a Shadow Inventory?

Housing Bubble 2.0

Shadow inventory in the housing market refers to properties will come to market but are not yet listed. While this inventory is based on estimates, it's important to understand its significance due to the impact on the potential future supply of homes for sale, which can significantly affect housing prices and market dynamics. We are going to go through analysis to understand where the current rental market stands and how it can impact the US housing market.

The Household Pulse Survey from census.gov gives some key insights into the rental market. When we examine the situation of renters who are behind on their rent, we observe an increasingly troubling trend. Over the past couple of years, the amount of overdue rent has grown, reaching an average of approximately 3 months of backrent for these tenants.

Upon further examining the likelihood of eviction among the same group of renters, we encounter an even more concerning trend. The percentage of tenants deemed very likely to face eviction has escalated from 16% to an alarming 23%.

It's important to highlight that there has been a gradual increase in the overall percentage of rentals paid on time, as illustrated below. The proportion of timely rental payments has risen from approximately 80% to 82.5%.

However, it's crucial to understand that this improvement is attributed to survivorship bias. The total number of rentals included in the study is decreasing, leaving only those tenants who are able to pay their rent. As indicated in the data below, the number of rentals surveyed has declined from approximately 62 million to 58 million, representing a decrease of 6.5%. (Unfortunately this study only goes back to 2020).

The insights from the Household Pulse Survey highlight a critical trend: as renters increasingly fall behind on rent and face higher eviction risks, and with a noticeable decline in the total number of rentals, there's potential for a significant shift in housing supply. This situation could lead landlords to convert rental properties into sales to mitigate losses from high vacancy rates and unpaid rent. This change in the supply dynamics can have a substantial impact on the housing market, affecting everything from affordability for potential homebuyers to investment strategies and overall market stability.

Additionally, there is corroborating data that supports the observations mentioned above. Rental prices are declining across the United States, with many areas experiencing negative growth rates. Specifically, year-over-year data for November 2023 indicates a decrease of over 2% in rental prices nationwide, with the trend showing a significant downward trajectory. Source

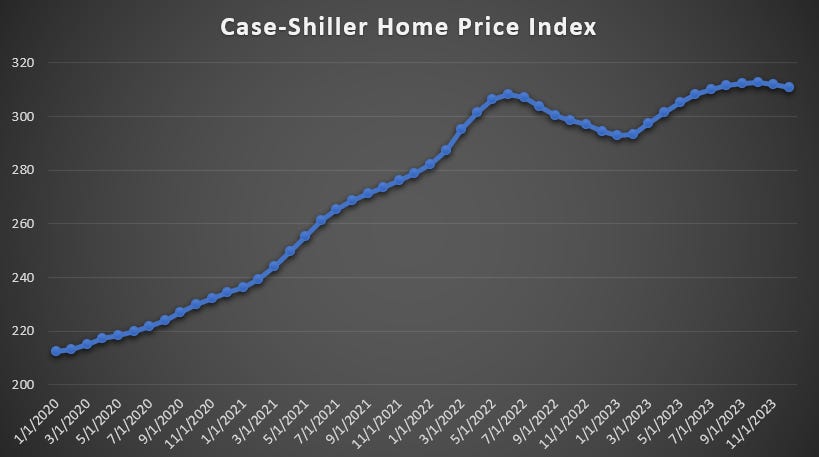

Case Shiller Home Price Index

The Case Shiller Home Price Index, which tracks changes in the value of residential real estate across several markets, shows a pattern that mirrors the stages of a typical asset bubble. There has been a major increase in housing prices, while prices have more or less stayed high. This sustained high level of prices has created a pervasive illusion among many that housing prices are immune to decline.

However, in the lifecycle of any bubble, there inevitably arrives a moment when prices begin to fall, ushering in phases of denial, fear, and ultimately capitulation. Homeowners rush to sell in an attempt to preserve their home equity before it dissipates. During this phase, the market often faces a scarcity of buyers, as the previously high prices have excluded many potential purchasers who are now hesitant to invest in a declining market, wary of "catching a falling knife." We are currently in this stage as evidenced by the sharp decline in existing home sales, as seen below.

Right now, the housing market's at a crossroads with two main ways it could go. On one hand, people's paychecks could start catching up to those steep home prices, making things balance out. On the other hand, and what seems more likely with how things are going, home prices might have to come down a notch to match what folks are actually earning. For housing prices to stay elevated, we'd need to see our incomes go up without our other bills piling up even higher.

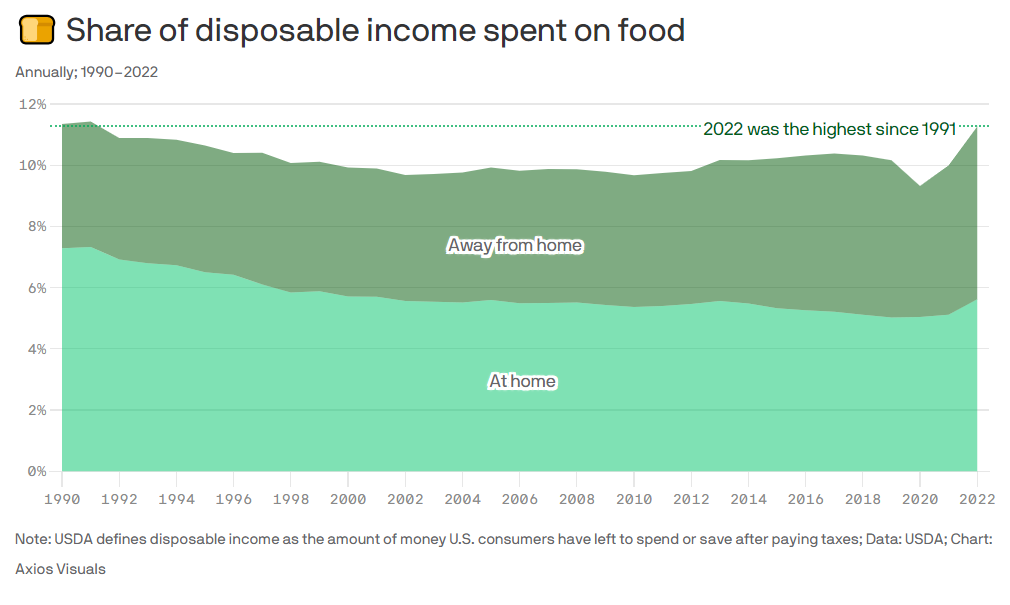

Here's some data to give us a clear picture of where the average American stands in terms of affording a home purchase or even just keeping up with their current mortgage payments.

Mortgage Payments: (Source)

% Of Disposable Income Spent On Food. (Source.)

Credit card delinquency rates have surged beyond the levels seen during the COVID-19 pandemic, a time when many were compelled to stop working. (Source)

Almost ~70% of Americans Cannot save money after their paychecks. 30% cannot even cover current expenses. (Forbes) Other Sources (Barrons, CNBC)

This collective evidence suggests that American housing prices are unsustainable given the current economic conditions. The rising expenses driven by inflation are not being adequately counterbalanced by wage increases, and mortgage payments are becoming increasingly burdensome amidst these escalating costs. Additionally, the growth of shadow inventory signals the potential formation of another housing bubble.

Thanks For Reading!

To Read Past Newsletters Click here.

If you have any source you wish to see in our lineup, please reach out and let us know. We continually look to incorporate more independent sources to our weekly wrap-up.