Treasury Yields Surge. Jobs Smash Expectations.

A Bear Steepening Further Signals Recession Warning

The recent surge in Treasury yields has sparked concerns among market observers, drawing comparisons to the 1987 stock market crash. In October of 87’, the Dow Jones Industrial Average plummeted 22.6% on what became known as Black Monday. The current situation is causing anxiety because the crash in 1987 was preceded by a sharp increase in Treasury yields, similar to what is happening now.

10y Treasury Yields In 1986 to 1988:

10y Treasury Yields 2022 to 2023:

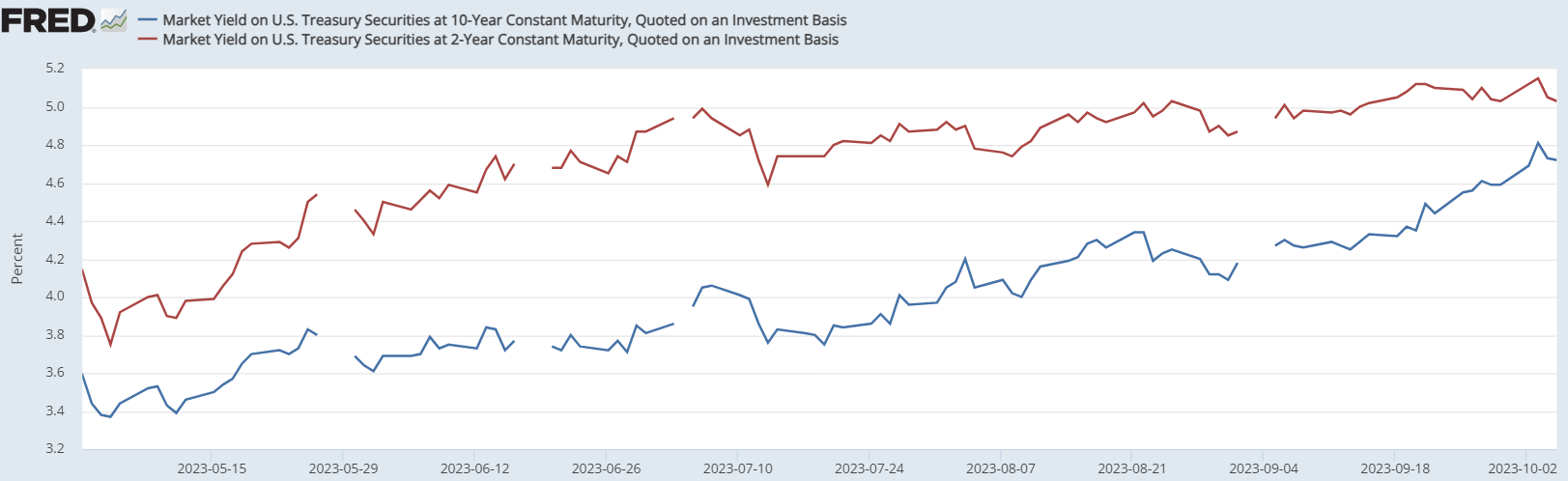

The recent spike in bond yields has led to a swift dis-inversion of the yield curve. The yield curve inverts when long-term debt instruments have a lower yield than short-term debt instruments. For 15 months, the yield curve has been inverted, which is one of the strongest recession indicators.

Before Article Market Predictions:

There are two ways the yield curve can un-invert. A bear steepener & a bull steepener. A bear steepener is where the long end of the yield curve goes up. A bull steepener is where the short end of the yield curve goes down. The bear steepener is seen as a warning sign for an impending recession. The inversion of the 10year - 2year reached 109 basis points at one time. This is the strongest signal of a recession that we have seen in over four decades. However, there is typically a lag between the inversion of the yield curve and the start of a recession, usually ranging from four to six quarters with an average of five.

Some experts argue that the inversion of the yield curve is more closely tied to policy rate hikes rather than market forces affecting long-term yields. In other words, they believe that a rate hike can actually cause a recession, and the inversion of the yield curve is simply a reflection of this. The time it takes for a rate hike to have an impact is also around four to six quarters, which aligns with the lag between the yield curve inversion and the realization of a recession.

BLS Jobs Report

The release of the BLS report led to a rise in benchmark 10-year US treasury yields to their highest levels in 16 years. In contrast to the bond and treasury yields, the U.S. job market experienced a significant boost in September, with the addition of 336,000 new jobs, surpassing the expectations of Wall Street. Furthermore, the employment figures for July and August were revised upwards, with 236,000 and 227,000 jobs added respectively. However, despite the increase in job creation, the unemployment rate also rose from 3.7% to 3.8%.

While the headline numbers seemed positive, there are underlying issues that need to be addressed. There was a decrease of 22,000 full-time jobs in September, following a reduction of 85,000 in August and 585,000 in July. Over a six-month period, full-time jobs have decreased by 172,000, averaging a net loss of 29,000 jobs per month. Much of the additional jobs being brought into the market are from part-time employment. Over the last six months, part-time jobs increased by 589,000, averaging an increase of just 98,000 per month. However, this increase in part-time employment does not compensate for the loss in full-time jobs, leading to significant economic challenges.

Earnings data also corroborates the troubling state of the labor market. Weekly earnings increased by just 0.2% for two consecutive months, following a 0.4% increase in July. This is the lowest increase since February 2021. On a year-over-year basis, weekly earnings in September increased by just 3.73%, the lowest annual rate since March 2020.

One interesting aspect highlighted in the report is the number of multiple jobholders. In September, there were 8.15 million individuals holding multiple jobs. The percentage of multiple jobholders as a proportion of total jobholders is currently at 5.0%. This is lower than before the pandemic, but has been trending up since the start of covid.

Despite the jobs being driven by part-time employment additions, the majority of reporting on the jobs report has been very positive with many believing this positive data is likely to push the Federal Reserve towards raising interest rates again by the end of the year.

Federal Reserve Rate Hikes

The president of the Federal Reserve Bank of San Francisco, Mary Daly, stated on Thursday that if the current economic conditions remain stable, the Federal Reserve may not need to raise interest rates further this year. This is due to the recent rapid rise in U.S. bond yields. The 10-year yield has already increased by 0.909 percentage points in 2023. Daly mentioned that the climb in rates on long-term Treasuries is essentially doing the central bank's job for it, potentially allowing them to avoid lifting interest rates further.

Daly emphasized that the Federal Reserve's aggressive efforts to control inflation since last year have brought the benchmark interest rate to its current level of 5.25% to 5.5%. She stated that if the labor market continues to cool down and inflation returns to the target rate, they can maintain interest rates at their current level and let the effects of their policies continue to work. In the previous FOMC meeting, officials projected that unemployment would rise to 4.1% next year, down from an earlier projection of 4.5% earlier this year. Following the release of the jobs report, the odds of an interest-rate hike by the end of the year rose to 56%.

Yields Rising Implications

This bond market rout is the most significant in 150 years in terms of total returns. In 2022, US bond investors experienced their worst year since 1871, with a total return of -15.7%. The year-to-date return for 2023 has been almost -10%, making it even worse than the previous year.

With bond yields rising, the federal deficit is projected to exceed 7% of GDP in fiscal 2023, a shocking number for an economy that is close to full employment. The relatively short average maturity of the federal debt and the projected increase in budget deficits highlight the unsustainability of current fiscal policies.

The Treasury Department is now auctioning off more debt to cover the government's growing budget deficit, which reached $1.5 trillion this year and is expected to rise further in 2024. The U.S. Treasury plans to borrow $1 trillion in the July-to-September quarter and another $852 billion in the October-to-December quarter. As a result, the yield on the 10-year Treasury has spiked by 75 basis points in the third quarter, and the 30-year yield has risen even faster. The supply of Treasuries is increasing while the Fed is reducing its holdings of bonds. Overseas buyers have also reduced their purchases, leading to higher yields.

Looking ahead, issuance is projected to continue rising. Torsten Slok, Chief Economist at Apollo Global Management, anticipates an average increase of 23% in Treasury auction sizes in 2024. While the scale of borrowing has not caught bond investors by surprise, the market has only gradually adjusted to the relentless issuance.

Potential Collateral Crisis

Lenders are realizing that collateral values are likely to continue falling, especially for longer durations, and that excessive leverage is a recipe for disaster. This leverage has been exacerbated by the ability for collateral to have multiple claims of ownership.

The Depository Trust and Clearing Corporation (DTCC) has created a dematerialization of securities from certificate form into book entry. The DTCC also operates a securities financing transaction clearing facility, which introduces central clearing for equity securities financing transactions such as lending, borrowing, and repo. This service aims to support central clearing of institutional clients' equity transactions intermediated by sponsoring members and between full-service NSCC members. This creates pools of collateral available to institutions without the knowledge of securities entitlement holders, the DTCC effectively creates another claim on these assets. This means collateral like stock certificates can have multiple owners for every share.

Not only does this situation seem immoral it creates systemic risk. When multiple financial institutions are interconnected through collateral arrangements, a crisis affecting one institution can quickly spread to others. If a significant number of borrowers or lenders face difficulties in meeting their obligations, it can lead to a broader financial crisis because of the leverage being applied.

After Article Market Predictions:

For more analysis on these topics, check out these articles:

Why an Un-Inverted Yield Curve Could Be More Chilling for the Stock Market

Fed Will Lean Toward Another Rate Hike After Blowout Payrolls

Jobs report shows big 336,000 gain in hiring in September. Labor market still hot.

Mixed messages behind the headlines of a blowout US jobs report

Charting the Global Economy: Strong Data Send Bond Yields Surging

Shocking New Jobs Numbers Just Released...You Won't Believe This

Bond Yields, Oil Prices, Fed Rates Have All Sparked Gloom. Why Theres Optimism.

The Fed Might Not Have to Hike Interest Rates Again, Fed Official Says. Thank Rising Bond Yields.

Stronger than expected jobs market raises fears of US interest rate rise

Thanks For Reading!

If you find value in this newsletter and want to make sure you don't miss any important updates, you should definitely consider subscribing. By subscribing, you'll be the first to know about new articles and special offers.